By: Chapin Flynn, Max Barnes, Alice Huang, Dustin Goldberg, Elsa Jensen, Julia Martin and Nitya Maddineni

Published: August 21, 2024 | Updated: August 21, 2024

Read time: 9 minutes

- Table of contents

Introduction

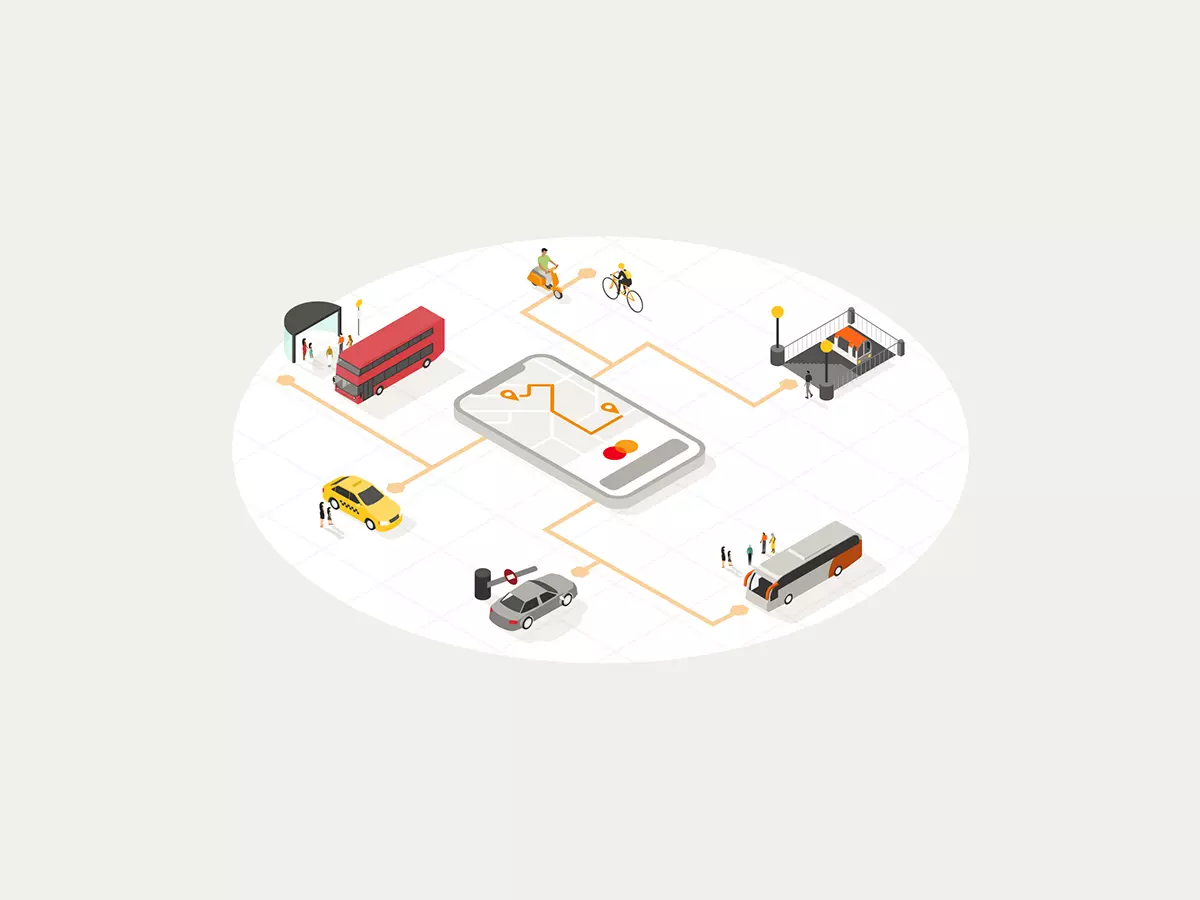

Imagine living in a country where all modes of transit — trains, buses, cars, and more — are connected via the same seamless payment systems as retail payments.

Gone are the days of digging for separate transit cards or fiddling with a smartphone to access a bike share

Public transit users need only tap in or out with their “open-loop” payment method to access public transit. Bike users can take a rental bike with just a tap of their card, no account or application needed. Drivers who need to pay to refill their electric vehicles can do so seamlessly by simply tapping their card.

Gone are the days of digging for separate transit cards or fiddling with a smartphone to access a bike share. Even visitors can pay with debit and credit cards, physical or digital, just as easily as locals. Accessing transport is seamless and efficient for everyone.

In December 2012, Transport for London (TfL) worked with Mastercard to make open-loop transit a reality by implementing contactless payments on London’s buses. Just under two years later, TfL expanded the payments to the London Underground trains.

Many cities followed London’s lead, but it was not until over a decade later that a country implemented a similar system nationwide. In June 2023, Translink, a Dutch multi-operator ticketing system, along with public transport operators (PTOs), partnered with Mastercard to implement a nationwide open-loop system in the Netherlands.

Around the same time, the Maldives Transport & Contracting Company (MTCC) and Bank of Maldives partnered with Mastercard to implement open-loop payments on its nationwide bus and ferry system in the Maldives. The varied approaches to the Netherlands’ and the Maldives’ nationwide transit systems provide case studies for global PTOs and governments.

Further insights come from other collaborations around the world. From dual-purpose transit debit cards in Bogotá to new payment solutions for electric vehicle chargers in Europe and tap & ride e-bikes in Lahti, Mastercard's expertise, data, and custom solutions have revolutionized urban mobility.

Open-loop contactless transit payments in the Netherlands

The Netherlands’ nationwide public transport system is unified under Translink, a comprehensive multi-operator ticketing system, and comprises PTOs, validators, issuing and acquiring banks, advocacy groups, governments and supervisory bodies.

- Further reading:

How financial institutions can enable sustainable consumption

How payment card popularity lays a pathway to sustainable consumption

Evolution of OVpay

In 1980, the Netherlands introduced the Strippenkaart, a paper-based ticketing system employing strips representing different travel zones. Two and a half decades later in 2005, the Netherlands transitioned to a more advanced ticketing solution: the OV-chipkaart or “OV chip card.”

This contactless, closed-loop card system, powered by MIFARE technology, eliminated the need for physical ticket stamping. It also offers automatic reloads and uses a convenient check-in and check-out process, where travelers tap their cards at the journey's onset and conclusion. Fares are calculated based on distance traveled, and the card supports traveler-specific subscriptions and discounts.

Yet Dutch travelers, like their counterparts in London and elsewhere, are increasingly demanding more convenient ways to pay. In response, the Netherlands introduced the next evolution in its public transportation system: OVpay.

OVpay is an open-loop contactless payment system, powered by EMV technology, that allows travelers to conveniently tap in and out using their physical or digital debit or credit cards across all modes of public transport. Fares are seamlessly charged to the linked payment method by a single merchant, while passengers can easily access detailed payment summaries through the OVpay website or app. This technology makes the Netherlands the first country to implement an open-loop transit payment system nationwide.

A centralized fare collection entity, managed by Translink, streamlines backend operations. Translink collects fares on behalf of PTOs, then transfers funds from the cardholder's issuing bank to Translink's acquiring bank, and finally distributes revenue to each of the PTOs.

Taking a holistic approach to implementation, Mastercard worked closely with multiple players in the Netherlands' transport ecosystem. As the nationwide transition to OVpay unfolded, Mastercard collaborated closely with Dutch national and commercial banks to ensure the effective implementation of mobility transaction processing rules.

As a primary infrastructure player, Mastercard collaborated with acquirers and financial institutions to ensure that all validators were equipped with the software and components for seamless countrywide transactions. Mastercard’s consulting team also helped optimize functionality by bringing together thousands of acquirers to enhance approval rates and troubleshoot declines, assisting with the migration from existing cards to new ones, and providing a marketing toolkit to drive adoption.

Impact of OVpay and looking ahead

The Netherlands' nationwide implementation is a groundbreaking step in urban mobility. From its inception in May 2022 to January 2024, the number of taps reached around 22 million, according to official numbers from the OVpay 2024 report.

The shift in transaction dynamics is particularly remarkable: while OV-chipkaart payments previously captured 100% of transactions, OVpay has swiftly captured 15.2% of transactions through EMV taps and 27% from full-fare adoption of debit and credit cards as of June 2024, according to the report. Customers have responded enthusiastically, reflected in a customer satisfaction score of 8 out of 10, according to an official OVpay survey.

Looking forward, Mastercard intends to continue supporting the roll out of open-loop contactless payment systems, such as OVpay, to maximize reach and impact. Later this year, OV-pas, the second payment method within OVpay, will be introduced. OV-pas is a closed-loop token solution designed for individuals with subscriptions and students, according to the OVpay report. By 2025, the Netherlands will be migrating from OV-chipkaart to OVpay, phasing out MIFARE technology and transitioning fully to EMV technology with a strong focus on open-loop solutions, according to the report.

Open-loop transit payments in the Maldives

In 2021, the government of the Maldives signed a contract with the Maldives’ Transport & Contracting Company (MTCC) to operate the national transit system, the Raajje Transport Link (RTL). RTL is unique in using buses and ferries to connect the hundreds of atolls and islands across the nation for locals and tourists.

That same year, MTCC, the Bank of Maldives (BML), and Aurionpro Transit, which provides automated fare collection technology, partnered with Mastercard to implement a new, multi-modal open-loop transit payment system for RTL — the first of its kind in South Asia.

Although the Netherlands and the Maldives both instituted open-loop transit systems, the two implementations differed because of socioeconomic factors

The open-loop system was launched in September 2021, followed by an option for QR code ticketing in September 2022, contactless payments in January 2023, and an upcoming launch of a cobranded RTL prepaid card. The prepaid card is particularly beneficial as it promotes financial inclusion for unbanked and underbanked customers, allowing them to still use public transport despite the move to an open-loop system.

Although the Netherlands and the Maldives both instituted open-loop transit systems, the two implementations differed because of socioeconomic factors. Nearly a third of the Maldives’ GDP comes from tourism, according to numbers from the US department of state, whereas less than 4% of the Netherlands’ GDP comes from tourism, according to the World Travel & Tourism Council.

Additionally, the Maldives recorded roughly 14 million RTL rides across all modes of transit in 2023, while the Netherlands saw 1.1 billion public transit rides during the same year, both according to government figures. Given the Maldives’ reliance on tourism, it is critical that visitors can easily access public transit.

Mastercard’s Role

Throughout the RTL implementation, Mastercard supported MTCC with Mastercard Payment Gateway Services (MPGS) and consulting engagements. MPGS acted as the payment service provider, while the consulting team concurrently covered five workstreams: project management, card value proposition and customer journey development, technological integration, go-to-market strategy, and customer service training.

MTCC, in collaboration with Mastercard, structured the implementation in two phases, starting with the planning and rollout of QR tickets on RTL before moving into the second phase focused on open-loop card issuance, EMV acceptance on RTL, and the co-branded prepaid RTL card. Many of the steps were similar but tailored to their respective technologies — QR codes or open-loop payments.

| Phase 1 | Phase 2 |

| QR code ticketing | Open-loop payments & co-branded cards |

|

|

The Netherlands previously employed a closed-loop transit card, so the nation primarily transitioned directly from closed-loop to open-loop cards. In the Maldives, however, passengers used to pay in cash or use bus cards, albeit with few places to refill them. Therefore, MTCC and Mastercard focused less on card migration and more on initial adoption. The second phase of the engagement concluded with a pilot launch of the open-loop system, and a Mastercard project management team stayed on to help facilitate the full rollout.

Despite the differences between the approaches in the Netherlands and the Maldives, the RTL and OVpay open-loop systems and implementations share many similarities. In both cases, transit authorities and local banks collaborated with Mastercard for help implementing the systems and for technical and strategic advice with a particular focus on marketing and card acceptance. Additionally, both nations ensured that unbanked and underbanked riders could still use public transport regardless of the method of payment.

Additional involvement in the urban mobility space

Dual-purpose payment cards in Bogotá

Bogotá's Integrated Public Transportation System (SITP) serves millions of commuters daily. The preexisting payment system, the Tullave smartcard, required frequent reloading, which led to long lines and delays as the infrastructure struggled to keep pace with the city's growth, leading to congestion and inefficiencies in the transit system.

The card issuer Bancolombia Bogotá decided to work with Mastercard to launch a dual-purpose payment card solution to integrating transit payment functionality into credit or debit cards issued by Colombian financial institutions. In February 2015, Bancolombia launched the first such card to enable contactless payments for both retail and transit fares.

In its first year, the Bancolombia Mastercard’s rate of card issuance averaged double-digit growth each month, and nearly a quarter of the cards were activated for SITP usage. Financial institutions in other Colombian cities also adopted the model, leading to reduced waiting times at top-up kiosks, lower fare collection costs, and increased financial inclusion.

Tap & go in Manila

In February 2024, AF Payments and Mastercard collaborated to work on enabling contactless acceptance of Mastercard cards on Manila’s buses and part of its Metro Rail Transit System. The initiative will allow travelers to tap their prepaid, debit, or credit cards and eliminate the need for separate tickets. While still currently in pilot phase, the goal is to roll out the initiative across other modes of transit in Manila and eventually throughout the country.

Freebike in Lahti

In 2024, Freebike launched e-bikes enabled with a contactless payment functionality in Lahti, Finland, to promote public micromobility. Traditional bike-sharing systems often require users to have preexisting app accounts or register on the spot, a process that can deter potential users with its time-consuming nature.

Freebike addressed the issue by enabling a new payment method in collaboration with Mastercard, which allows users to simply tap their bank cards to access bikes without the need to register. The impact saw a significant increase in ridership within a month. The initiative plans to expand to other mid-sized cities around the world with cycling-friendly infrastructure and weather conditions.

EV charging and car payments in Europe

Currently, electric vehicle chargers often require a mobile application, a physical card, or a membership. In 2024, Last Mile Solutions worked with Mastercard to create a universal payment terminal solution in Europe that eliminates existing barriers and ensures interoperable payments for frictionless EV charging.

Additionally, companies like Ryd are making in-car commerce a reality by allowing drivers to pay for gas, tolls and soon for EV charging directly from their vehicles and mobile apps. As connected vehicles become more prevalent, seamless and secure in-car payment experiences can minimize congestion in urban environments. Similarly, quick and painless EV payment processes can help boost adoption of electric vehicles.

Conclusion

Mastercard embarked on its mobility journey over a decade ago with the aim of creating scalable and frictionless urban mobility solutions to simplify rider journeys worldwide. Along the way, major cities around the world have collaborated with Mastercard in the successful implementation of open-loop solutions while still maintaining flexible access for unbanked and underbanked populations.

Looking forward, Mastercard will continue to innovate with governments, PTOs, financial institutions, and regulators around the world. From improved EV charging stations to streamlined road tolls, Mastercard will keep working to enhance transit solutions for seamless urban mobility.

Contact us to learn how Mastercard enables scalable and seamless urban mobility for everyone, everywhere.

Related resources