The debit card shouldn't be overlooked. Banks must build customer loyalty, widen cross-sell opportunities and increase adherence to new digital payment services at a time when competition from other banks and fintech companies is on the rise.

In recent years, U.S. issuers have focused their efforts on expanding their credit card portfolios with eye-catching sign-up bonuses, cash back on purchases and luxurious travel perks — but failing to place enough emphasis on driving loyalty through debit cards might mean leaving opportunities on the table.

With banks offering such tempting rewards around credit card use, it's no wonder that U.S. credit card spend surged 10% in 2017 from the previous year, faster than any other form of card payment, according to the U.S. Federal Reserve's latest payments study. By comparison, debit card spending grew only 6.5%, which might explain a tendency for banks to underutilize their debit portfolios.

Building Customer Loyalty

A growing body of research shows that highly active debit cards drive overall customer engagement, strengthening a bank's relationship with its customers and increasing their loyalty. Indeed, according to the U.S. Federal Reserve, debit cards are the typical payment choice for a $10 purchase at a local store for 37.1% of respondents, compared to 24.3% of respondents who would typically use a credit card.

Optimizing debit portfolios and driving debit card usage can pay dividends beyond the value of additional transactions. A highly engaged current-account consumer can generate substantially more revenue for a bank by remaining more loyal and adopting multiple banking products.

Highly-engaged debit consumers are also big e-commerce shoppers, using both debit and credit cards, and they're more prone to want the latest technologies. According to Digital Transactions, a recent survey by Auriemma Consulting Group found that the use of debit cards is increasing for online and big-ticket purchases, a sign of rising consumer trust in e-commerce and confidence in personal finances.

Cross-Sell Opportunities

At the same time, debit can boost cross-sell opportunities for banks. The more a customer uses a debit card, the stronger their relationship is with the bank, and the greater the chance that they will expand the relationship to additional products and act as a brand advocate. As a result, banks can more easily migrate customers from initial checking and savings accounts to credit, loans, investments and new technologies like contactless and digital wallets. For example, if a highly-engaged debit customer decides to buy a home, the bank holding the debit account is more likely to be top of mind when shopping for a mortgage.

Hence, debit card usage is becoming one key indicator of the strength of the customer's relationship with their bank, which is vital for sustaining profits. According to Fiserv, a provider of financial services technology, "it's eight to 10 times more costly to acquire new customers than to sell additional products to ones you already have." If a customer with one product stays at a bank on average for 1.5 years, purchasing two products extends the relationship to four years, and with three products, it reaches 6.8 years, according to Fiserv.

A Staple That Shouldn't Be Overlooked

The advantages of debit are important for banks at a time when new competitors are continually emerging, such as fintech companies with low-cost, high-tech products.

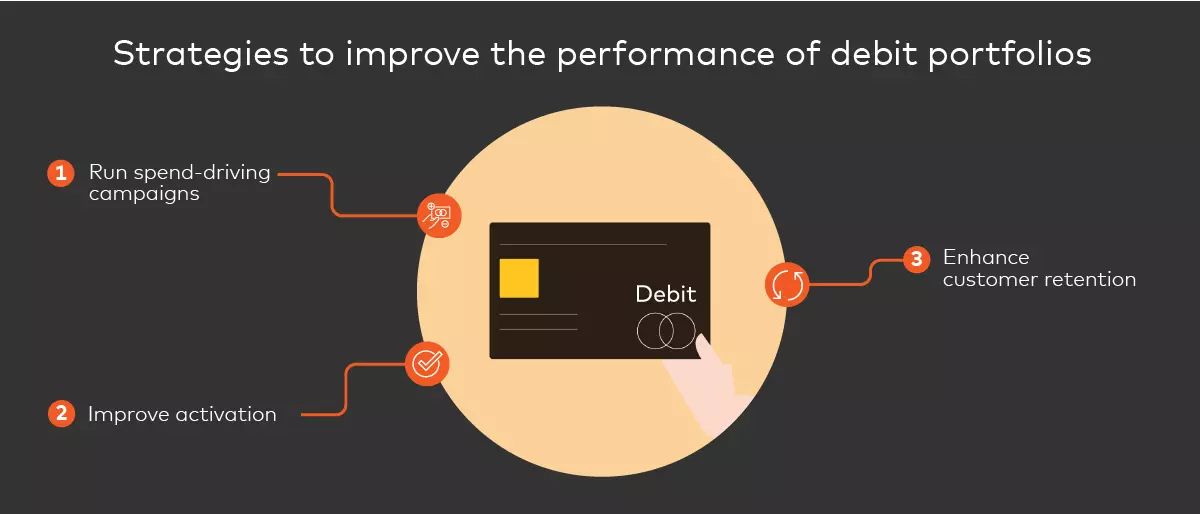

With this in mind, banks should focus on identifying opportunities to optimize debit portfolio performance, such as running spend campaigns, improving activation, and enhancing customer retention strategies. This will allow banks to unlock the full potential of their debit portfolios, helping not only to keep ahead of fintech startups but also to build life-long relationships that generate more revenue.