February 2023 | By Daniel Varkonyi

Part 2 of From backup singing to lead vocals: Payment acceptance moves to the forefront of payment technology.

The acronyms CP and CnP are familiar to most people with even a cursory interest in the mechanisms of card payments. Less familiar is how their definitions as card present and card not present gloss over a technical distinction between cards and cardholders.

For a long time, the distinction between card presence and cardholder presence did not really matter.

Cards were either read physically in the presence of cardholders as CP transactions, or card numbers were captured remotely as CnP transactions. The binary payment split between CP and CnP reflected a divide between brick-and-mortar retail and e-commerce.

But then brick-and-mortar retail and e-commerce began to blur along with any associated payments.

Consumer demand makes the blurring inevitable. The speed and smoothness of that march to the inevitable will depend on actions by acquiring banks and other payment service providers (PSPs) in partnership with retailers.

No line between online payments and offline payments

The story is no longer about how e-commerce disrupts brick-and-mortar but about how they work together in an omnichannel experience. The implicit understanding that card presence or absence goes hand in hand with cardholder presence or absence no longer holds tight.

Online payments have grown considerably in recent years. In the third quarter of 2021, card-not-present volume on Mastercard-branded programs was at 145% of the comparable 2019 amount. Yet the stat is liable to misinterpretation. The use of the term card not present follows the standard practice of not indicating whether cardholders are physically present or not. And where online growth would once have been solely attributable to e-commerce, some of it now involves an offline component.

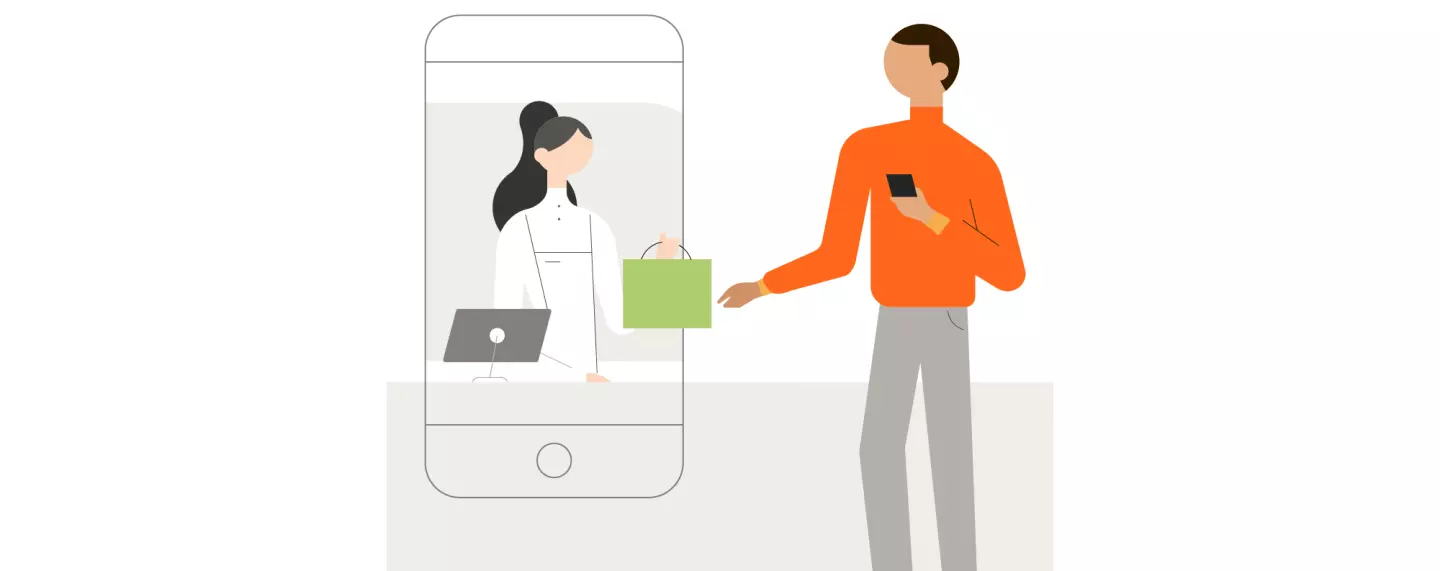

Perhaps the most salient example of online–offline blurring is “click & collect” or “buy online, pick up in store” (figure 1), but it does not affect the payment itself and disrupt the traditional association of CnP with cardholder-not-present.

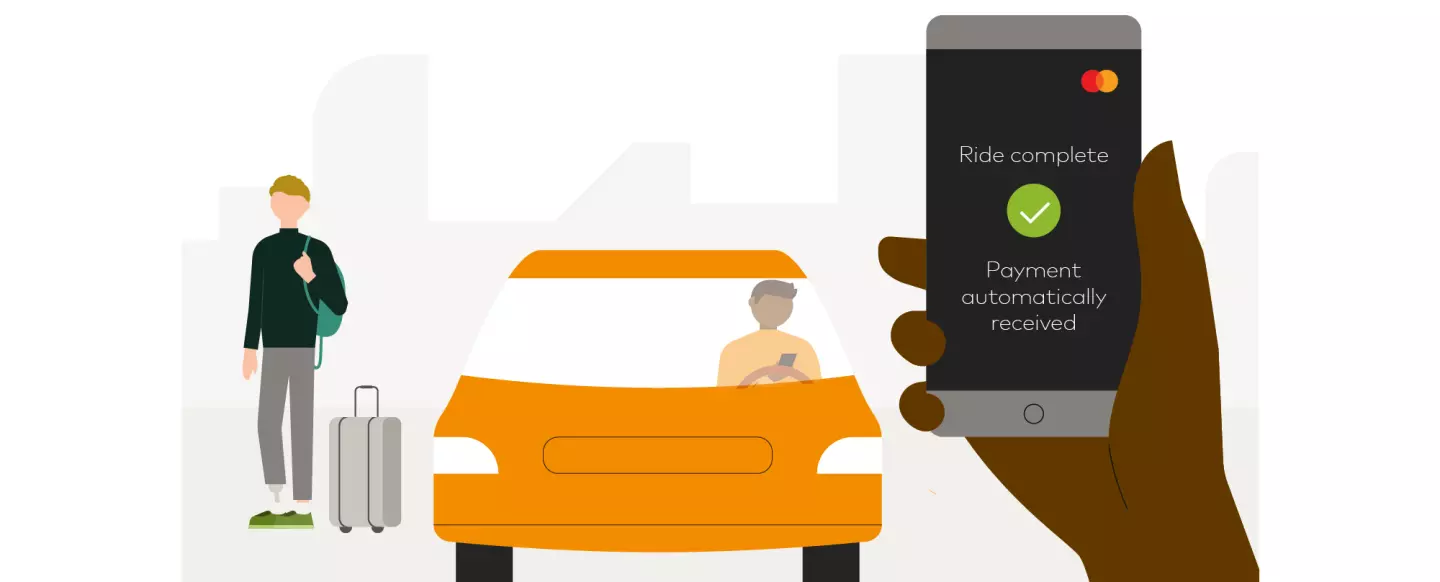

A more fundamental blurring now comes from how consumers may access e-commerce physically in store. Mobile devices and in-store technology let physically present cardholders make CnP payments.

That nullification of an exclusive association between cardholder presence and CP payments comes via an evolution in the use of cardholder credentials.

Redefining card-on-file transactions

A standard definition of card on file (CoF), perhaps more appropriately known as credential on file, is cardholders storing their payment card information online with retailers. As an online capability, it traditionally covers payments without physical cardholder presence.

Yet as payment technology advances and the online–offline distinction blurs, the definition of CoF is evolving. Digital wallets, including Click to Pay offered by major payment networks online, represent a form of CoF that is not necessarily tied to individual retailers (figure 2).

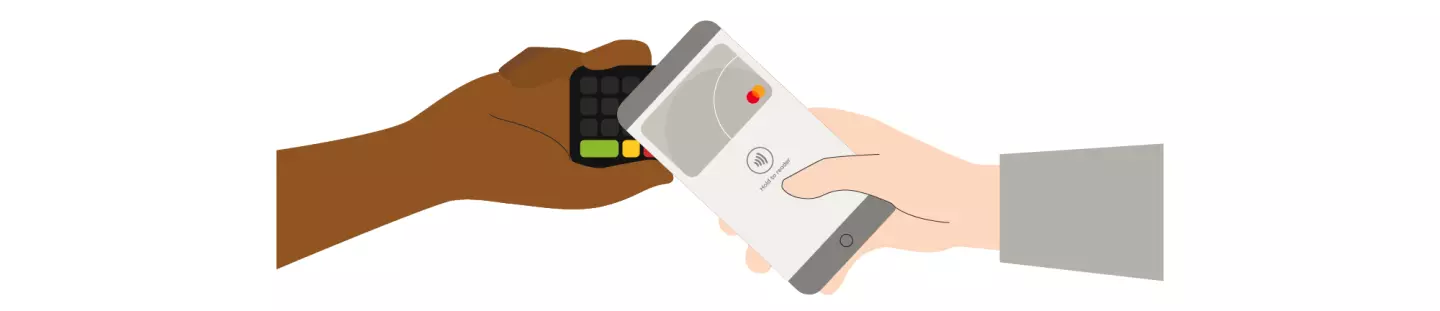

Digital wallets that can be combined with the near-field communication (NFC) technology used in contactless cards now let cardholders “tap to pay” with mobile devices (figure 3).

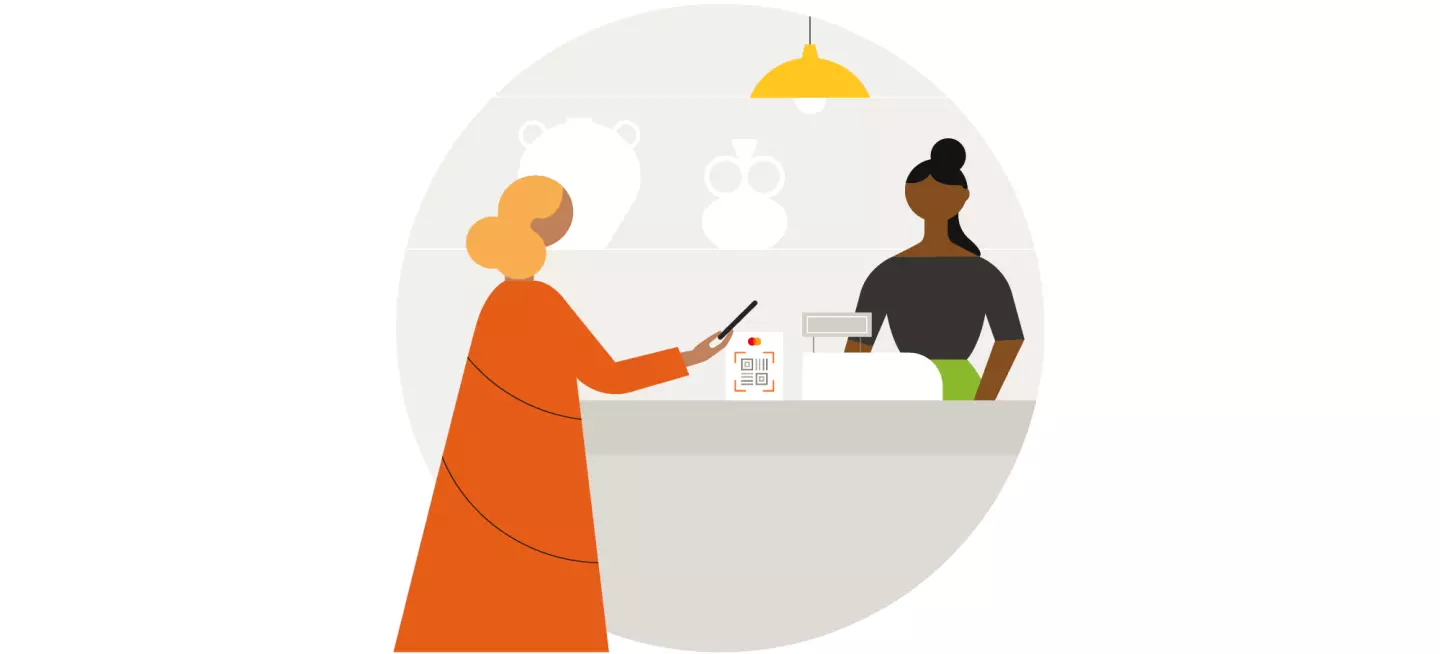

Alternatively, QR codes let cardholders “scan to pay,” which can also be used for payment on delivery without needing a portable payment terminal (figure 4). The result is something that would have seemed oxymoronic only a few years ago: CoF with cardholder presence.

Invisible transactions are now evolving CoF even further as embedded payments. Permissioned credentials may simply be accessed at the time of service, such as when a cardholder enters a checkout-less store or a rideshare vehicle. Biometric solutions, used by 48% of consumers surveyed worldwide in Mastercard’s New Payments Index, add further smoothness and convenience (figure 5).

The automatic population of a checkout page via CoF no longer just improves online experiences. It can also help offline by reducing checkout lines or eliminating them entirely. Shoppers are less likely to abandon their shopping carts—physical or virtual—in a truly omnichannel payment experience.

Blurred payments, clear opportunities

The main opportunities in the payment acceptance ecosystem lie in establishing where and how to help retailers by providing comprehensive omnichannel support. Approaches should span physical terminals and online gateways, extend across loyalty programs, encourage card use in emerging gig economies or where cash persists in established economies, and function cross border as well as cross channel.

When in-house technological development is impractical, partnerships with specialized technology companies are often the best way to cater to the myriad options. The key is to keep the complexity, ranging from device sensing to voice activation, behind the scenes while letting cardholders effortlessly flit between channels across one centrally orchestrated solution.

Traditional staples—such as the processing, underwriting and clearing of payments—might not be the focus, but smooth acceptance on the frontend necessarily requires a smooth backend. That also includes cross-channel payments reconciliation along with cross-border licenses and multi-currency settlement.

Frontend and backend technological improvements aside, the real challenge is around securing consumer confidence in the solutions. The credential-led transformation of payments comes with the caveat that CoF may as well stand for concern over fraud. Globally, 72% of consumers agree they are concerned about their saved card details being compromised, according to a Mastercard study in December 2019. In addition, if payments become too easy, consumers may fear a loss of control around accidental purchases and then dispute more payments.

Until a tipping point is reached in adoption, reassurance will come from acquiring banks and other payment service providers working with card issuers and retailers to communicate benefits to cardholders. Two areas stand out: the replacement of cardholder credentials with non-sensitive tokenized surrogates that reinforce CoF security and make cards less vulnerable to fraud, and the ability to predefine which retailers at what spending levels may go on a list of trusted beneficiaries to bypass additional authentication.

The story of retail payments used to be about offline brick-and-mortar versus online e-commerce. The convergence of CP with CnP and a reformulation of CoF is now shifting focus onto two new protagonists: blurred payment flows versus traditional payment flows. Acquiring banks and other payment service providers might consider shifting their approaches accordingly.

| Daniel VarkonyiPrincipal, Mastercard Advisors |